From the time that Oroco got involved with Santo Tomas, the investment thesis appeared to be very complicated. There were lawsuits in three different jurisdiction and etc. However, for those who took the time to study the details, the thesis was not complicated at all. It was complicated only for those that did not take the time to study the situation.

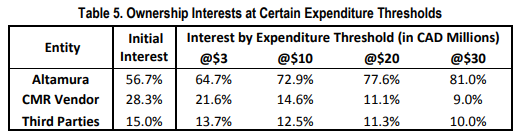

Right now, the ownership structure appears to be complicated. Again, if you take some time to study the details, the situation is not complicated at all. Here is the current ownership structure.

Altamura is Oroco. CMR Vendor is Ruben Rodriquez. Third Parties is people who helped with the lawsuit. As of now, Oroco own 56.7 percent, Rodriquez 28.3 percent, and Third Parties 15 percent. When Oroco spends CAD $3 million on the property, its interest grows to 64.7 percent while the interests of the other two parties get diluted. When Oroco spends CAD $30 million, it earns 81 percent interest in the project while Rodriquez remains at 9 percent and Third Parties at 10 percent.

So it appears that if a major bought Santo Tomas for $300 million right now, Oroco would only receive $170 million which would translate into

$170 million/157 million shares = $1.08 per share or CAD $1.41 per share

This is not correct.

Oroco has an option to buy out Rodriquez’ interest for $18 million. Here are the terms of the option. Clock starts ticking when Santo Tomas gets registered to Xochipala Gold.

12 months: $1 million

24 months: $3 million

36 months: $14 million

Total: $18 million

If Rodriquez interest is 28.3 percent, 21.6 percent, or 9 percent, Oroco can buy him out for $18 million.

Now that we understand this, let’s go back to the scenario where a major buys Santo Tomas for $300 million. At that time, Oroco would buy out Rodriquez for $18 million erasing his 28.3 percent ownership. Therefore, Oroco’s ownership gets to 85 percent.

$300 million buyout x 85 percent = $255 million/157 million shares = $1.62 per share or CAD $2.11

This is pretty good and note that no drilling took place. While the ownership structure shows that Oroco own 56.7 percent today, it is really 85 percent when we include the $18 million option to buy out Rodriquez.

Let’s go a step further. Let’s assume that no major is ready to buy Santo Tomas right now because they want to see confirmation drilling and/or they would rather pay more for Santo Tomas. In this scenario, Oroco raises CAD $13 million. This takes the share count to 185 million but it also raises the price of Santo Tomas to $500 million.

Spending CAD $13 million raises Oroco’s ownership to 72.9 percent and dilutes Rodriquez to 14.6 percent and Third Parties to 12.5 percent. Oroco can still buy out Rodriquez for $18 million. So now Rodriquez is at 0 and Third Parties still at 12.5 percent. Oroco is at 87.50 percent.

$500 million buyout x 87.50 percent = $438 million/185 million shares = $2.36 per share or CAD $3.07 per share

If the majors are stupid enough to let Oroco spend CAD $30 million on the property, then Santo Tomas will have compliant 43-101, feasibility study, and higher NPV. By then copper price will likely to be $4 per pound and NPV will probably be between $3 and $5 billion.

Oroco’s interest will only reach 90 percent. Rodriques will be bought out for $18 million. Third Parties will be diluted to 10 percent. Let’s see how the numbers look with different buyout prices.

$1 billion x 90 percent = $900 million/200 million shares = $4.50 per share or CAD $5.85 per share

$2 billion x 90 percent = $1.8 billion/200 million shares = $9 per share or CAD $11.70 per share

$3 billion x 90 percent = $2.7 billion/200 million shares = $13.50 per share or CAD $17.55 per share

CONCLUSION

As you can see, Oroco’s stock price will reach between CAD $2.11 to CAD $17.55 per share depending on three variables: drilling, majors’ speed, and copper price.

If a major buys us out right now, drilling does not happen, the price tag for Santo Tomas may be $300 million and we get CAD $2.11 per share. This is in theory because I doubt that the management would take CAD $2.11 per share. I would not take this deal.

If the majors want us to drill some, we will be successful because we are drilling into a deposit that already proved to be economical. The price tag goes up to at least $500 million and we get CAD $3.07 per share. I would take this deal.

However, if the majors are really generous and let us complete the feasibility study, then the price tag can go to between $1 and $3 billion and we can get up to $17.55 per share. The long term fundamentals for copper are stellar so the longer the majors wait, the better for us.

MARIUSZ YOU ARE CRAZY

CAD $17.55 is 44 times the current stock price. You are insane.

When I got involved in Oroco, the stock price was at $0.02. Then, I saw it go down to $0.01. Now the stock price is 40 times higher. It is the idiot sellers that created 40x opportunity. Now, it might be the majors (and current sellers) that can create another 40x opportunity. If they let Oroco spend CAD $30 million on the property and copper price goes to $4 per pound, then 40x is not just possible but very probable. It all depends on when they want to write the check.

Disclosure: Long Oroco